Full-service banks could lose 35% market share to #GAFA (Google, Apple, Facebook, and Amazon) and FinTech startups in the next 5 years. (Accenture) Will you be losing market share or gaining it?

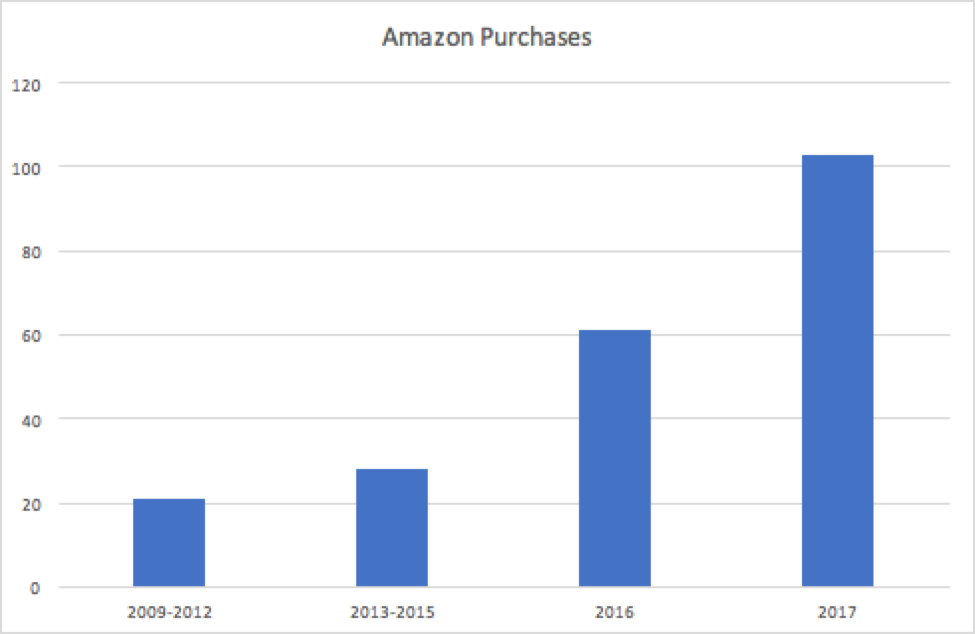

On December 15, 2009 my wife and I received our first package from Amazon. In the days and weeks leading up to the delivery of this package my wife and I scoured the shelves at Target, Walmart, and any other place in town to find “Scrooge,” the 1970 Albert Finney retelling of Dicken’s classic “A Christmas Carol.” This was to be our first Christmas together, and we weren’t going to make it through without reliving one of my wife’s favorite Christmas traditions, watching “Scrooge.” With a sense of defeat, and in a last ditch effort, we turned to Google and stumbled across Amazon. Lo and behold, our movie was available for just $8.58 and it could be shipped within 2 or 3 days. The “Scrooge” tradition had been saved by a company we had heard a lot about, but never used before - Amazon. This is where our relationship with Amazon began – and the graph below shows how our relationship with Amazon has changed over time.

A recent article from The Verge stated that Americans trust Amazon about as much as they trust their bank. Companies like #GAFA (Google, Amazon, Facebook, and Apple) were born in the age of software and the internet. The people running these organizations were technology visionaries and experts. Initially, #GAFA didn’t seem to pose much of a threat to the traditional financial institutions. How could a company that builds cool music devices called iPods impact a bank? How could a company that helps people find things on the internet hurt the financial institutions storing consumers money?

Hindsight bias makes this clearer for us today than it was when these companies were just starting. Seeing these trends early on and understanding the impact would have been incredibly difficult, but today it is becoming increasingly clear that companies like Amazon and Facebook may pose an even bigger threat to financial institutions than FinTech startups. In a recent study Accenture estimated that full- service banks could lose 35% market share to #GAFA and FinTech startups in the next 5 years and 79% of consumers see their banking relationship as merely transactional. (Source)

How will this happen? When consumers say things like “Why can’t my bank just be like Apple?” or “If I banked with Amazon, this would be so much better,” they are telling us that they have become so used to the simple, elegant experiences offered by #GAFA and other tech companies that they look with distain on anything that falls short of those experiences. Research corroborates that some consumers, if given the opportunity to drop their financial institution relationship in favor of banking with #GAFA, would do so in a heart beat (Source Accenture Banking2020 Report).

Cutting edge tech companies are pioneering the benefits of cloud computing, artificial intelligence, big data, blockchain, and ever improving customer experiences. They're tearing down the barriers to get people into saving money or sending money. They're creating better customer experiences by removing friction, leveraging data in incredible ways, and constantly researching what technologies can push their businesses to the next level. Meanwhile, financial institutions are often stuck years behind due to their legacy technology providers or because they lack the talent necessary to push the boundaries of innovation.

A few financial institutions are innovating well. The following were named to the top 5% of companies offering great customer experiences in their industries and regions in the 2017 customer experience (CX) index published by Forrester: USAA, Ally Bank, Navy Federal Credit Union, Huntington National Bank, and Regions Bank. As we examine what they have done, along with what the big tech players are doing, we can get a clearer picture of the steps financial institutions can take to grow their market share in the coming years.

Before we go much further I want to make sure you understand that this article isn’t all doom and gloom for financial institutions. Today financial institutions maintain a position of strength, but they're losing ground. I'm not a believer in the Blockbuster moment for banks. It will take time, but financial institutions need to act now. Here are a few things financial institutions can start doing that will generate real results.

1: Adopt a Growth Mindset

In order to make the necessary improvements, banks and credit unions must first adopt a growth mindset. In education a growth mindset is the opposite of a fixed mindset. Someone with a fixed mindset believes their intelligence or talents are fixed traits that cannot be expanded. People with a growth mindset believe their most basic abilities can be developed through dedication and hard work. This growth mindset helps create a love of learning and a resilience that is essential for great accomplishment. (Source)

Financial institutions with a growth mindset see technology as an incredible opportunity to grow and evolve their businesses - even if they don't fully comprehend it. They know there will be some painful moments, but they still experiment because they know the short term pain will help them learn the critical lessons they need in order to be successful. We do our best to limit the pain, but I am convinced that there can be no real growth without pain.

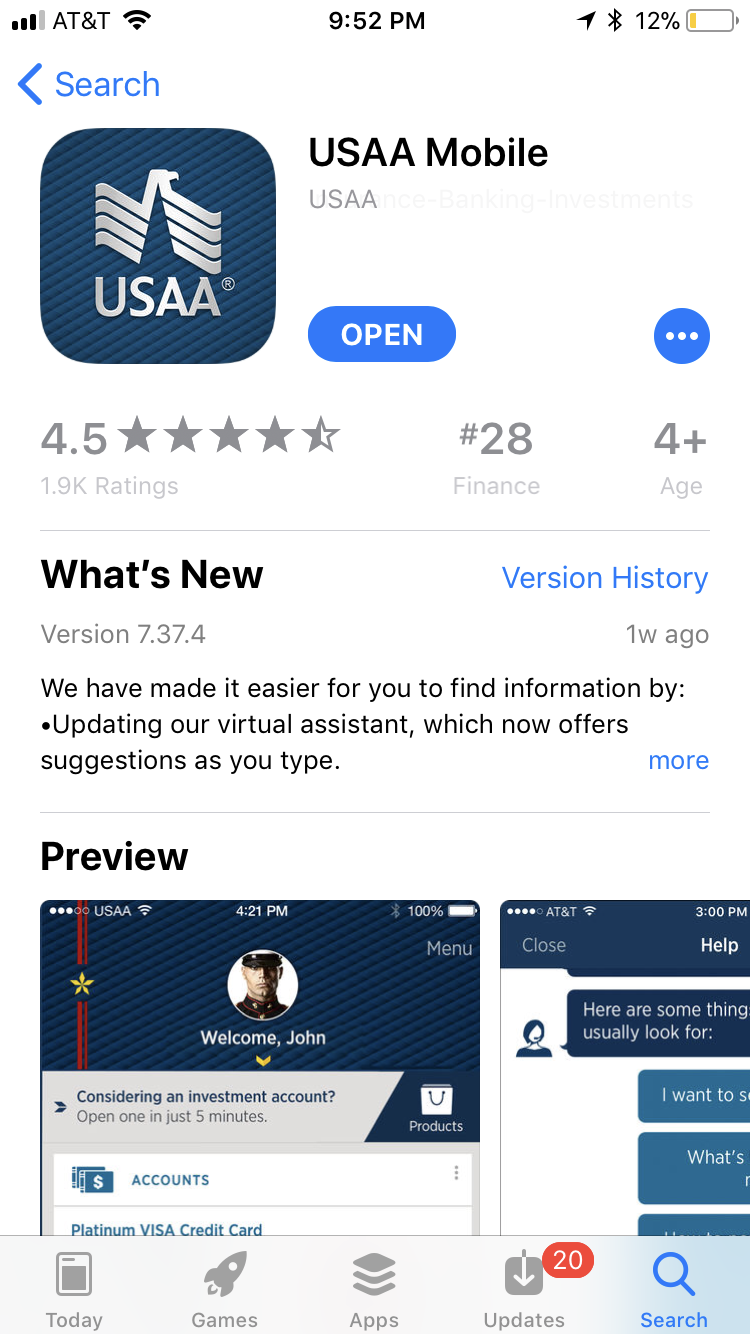

USAA's mobile app is a great example of this. They have obviously embraced the fact that they can do amazing things in the digital channel. Their app has almost 2,000 reviews and the average rating is 4.5 stars! They didn't start that way. They had to learn just like everyone else. Notice how they let people sign up with them right in their app. They're creating better user experiences by reducing the friction consumers have to go through in order to become one their customers - you don't have to go into a branch to setup an account.

A pivotal moment from the career of Andy Grove and Gordon Moore - two of the founders at Intel - helps demonstrate this point. In 1970, Intel created a low-cost memory chip that ended up being a huge hit; however, by 1985 Japanese companies were beating Intel at their own game. In what was certainly a difficult moment, Andy Grove turned to Gordon Moore and said “What would happen if somebody took us over, got rid of us - what would the new guy do?” Moore’s answer? “Get out of the memory business.” Some early experiments in microprocessing at Intel had yielded positive results, but memory chips made up almost all of their business at the time. Andy Grove agreed with Gordon Moore’s assessment that they should get out of the memory business, so they created a plan to change Intel from a computer memory company into a microprocessor company. This was an immense shift and it was certainly painful. They laid off almost a third of their workforce. But the success of their pivot is clear to anyone today. Grove and Moore were willing to ask some tough questions and make the changes necessary to position their company for a better future.

Are financial institutions having these sorts of conversations? It’s obvious that some people at financial institutions have had these conversations, because they're steering their financial institutions in a direction that challenges traditional norms or they’re out starting incredible FinTech companies right now. Why not foster these sorts of conversations inside your organization? Check out Under Armour’s website to see a fantastic example of an established company embracing change and inviting innovative people to help them create the future: http://ideahouse.ua.com.

2: Pick the Right Partners

Now you might be thinking “Jordan, this all sounds well and good, but if I listen to everyone claiming to know the next biggest technology in banking, I'd have a line a mile long out my door,” and I think you’d be right. I’m not proposing that we chase every rainbow, but we need to become well enough educated that we can quickly evaluate opportunities that come our way. Unless you're fortunate enough to have a Steve Jobs on your team to help you identify the right technology to invest in, all this talk of innovation and experimentation can be extremely daunting.

The bottom line is, your financial institution isn’t going to become Apple overnight – so let me throw in a plug here for great technology partners and your competitors. Every financial institution relies on technology partners in some way and most of us have relationships with competitors in our space. Here are some ideas to help you get the most from your organization, your technology partners and your competitors:

- Consider asking yourself or a colleague the following question: “If we were fired today and Steve Jobs was hired to fill our shoes, what would he do differently?”

- Ask your technology partners what sort of bets they’re making in the Open Banking space. If they don’t know what Open Banking is then that’s a good sign they’re not forward thinking enough.

- Ask a trusted partner or competitor what technologies they believe will play the biggest role in the next 5 years of banking. What are some experiments they've run in the last year that produced surprising results?

- Ask other financial institutions how much in-house development they do. If they’re doing in-house development, you could consider asking who their technology partners are and whether or not they have an API or SDK for your developers to access.

Asking these questions will help you begin to get a pulse on where things are today and where they’re headed.

3: Embrace Change and Innovation

Henry Ford famously said “If I had asked people what they wanted, they would have said: faster horses.” Here’s my plea as a FinTech entrepreneur to you, financial institutions and other financial services providers. We want to build tech that will make you more money, be relevant 10 years from now, and that helps you knock your account holders’ socks off, but we often need to shake things up a bit in order to get there. Please, join our conversations. We need to know what's off limits in the shake up and what's in bounds. Give us your feedback. Innovate with us and be willing to challenge some of the norms in our industry. You have knowledge that we need to succeed. We want to hear your challenges and we want to hear your creative ideas.

In 1910 I imagine there were a lot of people that saw a car break down on a dirt road in the middle of nowhere and said “I’ll stick with my horse, thank you very much!” We would all do well to step back and take a broader view of what is happening here. We need a growth mindset. Sure, the first car had its drawbacks. It may have initially even been worse than a horse for day to day transportation, but in a short period of time it became the technological marvel that we all use today.

We need to change our culture when it comes to innovation. We cannot have a fixed mindset in our businesses, believing our core competencies cannot be changed. We must adopt a growth mindset. We must believe that our core competencies can be improved through dedication and hard work. If the internet, AI, machine learning, and blockchain scare you then you’re totally normal! But you can’t stick with a fixed mindset. Real growth cannot come when we are only pursuing what we already know. Embrace your fears. You can learn this stuff!

Here are some things you can do now to help take financial services to the next level:

- If you work at a financial institution, call a progressive partner and ask them to host you onsite for a technology discussion. I recently sat in on a meeting like this here at Q2ebanking. It was an incredible!

- If you’re a progressive partner, invite customers onsite to learn more about the critical technologies that are shaping the future. Show them where you’re making your big bets and ask them where else you should consider making bets. Ask your partners for feedback on how these developments could impact them.

- Consider allocating budget each year for a few people to attend conferences like “Disrupt” (https://techcrunch.com/event-type/disrupt/) or “Money 20/20” (https://www.money2020.com/). These conferences often provide me with deep insight into where key technologies are today and where they’re headed.

- Make learning safe at your organization. Consider investing in a learning platform like lynda.com for your teams to use so they can come up to speed on technology. Help make it safe for someone to say something like “you know, I just don’t get this whole big data thing.” If it’s safe to make a comment like that, then it’s probably also safe to ask questions about how an organization is using big data. It’s probably also safe to spend some time learning about big data at an organization like that.

Conclusion

Financial institutions are core to our communities. Throughout the last 20 years the playing field has shifted in favor of the experiences provided by new technology providers. Unlike #GAFA, most financial institutions were founded and successful long before the advent of the internet – so it’s no wonder that a majority of financial institutions haven’t been able to use technology with the same effect as Google and Amazon. That said, it’s not too late to be part of the incredibly bright future in financial services – but it won’t happen by simply repeating the feature/functionality pattern created by legacy banking technology. By embracing the digital channel with a growth mindset, fostering innovation within your financial institution, and choosing technology partners that are investing heavily in the future, the next five years could be some of the greatest years of growth in your financial institutions history.